Viasat (VSAT)

Deep Analysis done: 1/24/22-2/1/22

Current Market Cap: $3.4 Billion

Share Price: 46.50

Before we get started this research file was compiled on Viasat only. In November they announced a deal to acquire Inmarsat for $7.34 billion including debt. This essentially doubles the size of the company. I will not be discussing the implications of this deal because it still has to go through the regulatory process and a firm knowledge of Viasat is needed to understand what this deal means. The merger will be discussed in a separate post.

Company Overview

Viasat (VSAT) is trying to connect the world by making reliable, high speed, cost-effective, internet available to all. To accomplish this mission they have spent the past 36 years building a broadband connectivity platform ranging from the big dishes you see along the highway to a satellite the size of a school bus located 22 thousand miles away in space. They revolutionized the use of high throughput satellites making the internet accessible to even the most remote places on earth like the battlefields of Afghanistan to 10,000 feet in the sky aboard Air Force One.

Co-Founded by Mark Dankenberg in 1986 VSAT got its start by providing “leading-edge technology for satellite networks and related digital communication products to the U.S Department of Defense” as they put it in their first public annual report in 1997.

Since then they have moved to become a vertically integrated end-to-end platform of high throughput satellites, ground infrastructure, and user terminals. This vertical integration has been part of the secret sauce at VSAT and is a big differentiator from their competitors. They keep most of the technological developments close to the vest, there has been a history of stolen IP (see the Hughes Juniper 2 satellite), and have a culture centered around customer innovation. The entire business is driven by seeing the demands of the customer and then developing and inventing the supply to meet those demands. This culture started in the beginning with the DOD contracts when they built products and hardware and has continued to evolve with the same mindset.

Here is their financial report card from roic.ai and I will warn you, this company doesn’t screen well

The current business operates in three segments, Satellite Services, Commercial Networks, and Government Systems.

Satellite Systems

In fiscal ’21 this segment generated $869 million in sales and earned $36 million in operating profit compared to sales of $826 million and $7 million in operating profit in fiscal ’20.

The satellite services segment is compromised of providing satellite-based high-speed broadband services around the globe. Their fleet of GEO stationary Ka-band satellites is at the core of the platform and right now they own 4 GEO satellites in the sky. 3 over North America; Wild Blue-1 launched in 2007, Viasat-1 launched in 2011, and Viasat-2 which was launched in 2017. They also acquired the remaining interest in a Ka-Sat over Europe, Middle East, and Africa (EMEA) from Euro Infrastructure Co during fiscal ’21.

In addition to the ones in the sky, they are currently towards the end of constructing their third generation of GEO satellites named Viasat-3. This global constellation is set to launch in 3 phases, The Americas, The EMEA region, and the Asia Pacific (APAC) region. The America’s satellite is set to launch in 4Q22 and with the second one to launch about 12 months after the first one, then it’s likely the same schedule will occur for the last one covering Europe, the Middle East, and Africa.

Launching and getting these three satellites into service is a big milestone and will change the entire economics for the company. These 3 satellites will now give VSAT global coverage, expanding their ability to deliver broadband all over the world. Above, I mentioned they provide broadband connectivity to the battlefields of Afghanistan, right now, they have to pay others to produce the bandwidth for the areas that are outside their current GEO reach. When Viasat 3 is in the air and operational, they no longer have to pay anyone else, those costs drop to $0, and the margins instantly expand.

In addition to expanding, their new castellation will bring 8x the amount of capacity onboard. When measured on a per-bit basis, this new captivity will slash the costs of producing one bit by about 50%. Thus giving them

1) A larger share of the broadband market if measured by the amount of total capacity in space.

2) The economic moat of being the lowest cost producer in a commodity type industry.

Launching Viasat-3 will be a massive disruption to the current industry and the culmination of years of hard work for the VSAT team.

The primary services offered in the satellite services segment are compromised of:

Fixed broadband services, providing high-speed internet to consumers primarily in the US as well as a few countries in Europe and Latin America. They also offer wholesale fixed broadband services to distribution providers. Right now they currently have around 590,000 residential subscribers.

In-Flight services, which provide in-flight connectivity to aircraft in the sky. This is how you can have Wifi on a flight from NYC to LAX. Right now they have about 1,490 tails n service and have customer agreements to add an additional 1,190 more in the future.

Community internet services, which offers the ability to connect places that have little or no other means of connecting to the internet. This is done through a community hotspot that is connected to the satellite. Since the launch of this service, they have been able to reach approx 2 million people in Mexico. They are currently trailing services in advance of a full commercial launch in Brazil, Guatemala, and Nigeria.

Other Mobile Broadband Services, like getting internet access to seagoing vessels, proving L-band connectivity which enables the machine to machine (M2M) probation tracking, are crucial for the management of remote assets and visibility into the supply chain. For example, being able to monitor Oil and Gas rigs, high-value assets tracking, and emergency responders.

Advanced Software and Communication Infrastructure, making it easier for companies to have ultra-secure connectivity and the industrial internet-of-things data enablement with machine learning. This division of the business primarily came into existence after the acquisition of RigNet.

Commercial Networks

In fiscal ’21 this segment generated $320 million in sales and lost 180 million in operating profit compared to sales of $344 million and ($186) million in operating profit in fiscal ’20.

This segment consists of developing and selling a wide array of advanced satellite and wireless products, antenna systems, and terminal solutions that enable access to high-speed internet. This line of system solutions provides products for all of the orbital regimes including, geostationary (GEO), medium earth orbit (MEO), and low earth orbit (LEO).

The commercial network segment is responsible for producing the hardware and ground infrastructure needed to enable satellite connectivity. It is the best place to see vertical integration at work.

Here is how management described it in their 2021 Annual Report:

“Our products, systems and solutions are generally developed through a combination of customer and discretionary internal research and development (R&D) funding, and products are often linked through common underlying technologies, customer applications and market relationships.

For example, products, systems and solutions developed and sold in our commercial networks segment are often complementary to those developed and sold to government customers in our government systems segment, and our portfolio of government and military offerings in our government systems segment leverages our technological investments in our commercial networks segment. Our commercial networks segment also drives growth in our satellite services segment. For example, the IFC terminals sold and installed on commercial aircraft and business jets in our commercial networks segment are then utilized to receive IFC services, driving recurring revenues in our satellite services segment”

The primary products, systems, solutions, and services offered in this segment are compromised of:

Mobile broadband satellite communication systems: designed for use in aircraft, seagoing vessels, and land-mobile systems.

Fixed broadband satellite communication systems: satellite network infrastructure and ground terminals.

Antenna Systems: state-of-the-art ground and airborne terminals, antennas, and gateways for terrestrial and satellite applications.

Space networking development: specialized design and technology services covering all aspects of satellite system architecture and technology.

Space Systems: the design and development of hah-capacity ka-band satellites and associated payload technologies for our satellite fleet as well as for third parties.

Government Systems

The Government Systems business has been called the crown jewel. This business unit earned $1.08 Billion in revenue in fiscal 2021 and produced an operating profit of $208 million. This unit alone accounts for about 45% of VSATs total revenue. As a whole, the US government alone has been the largest customer of VSAT and accounted for about 30% of total revenue for the past 3 fiscal years.

They are the leading provider of innovative communications and cybersecurity products and solutions to the U.S Government and their military and government users around the world. This segment offers a broad array of products and services designed to enable the collection and transmission of secure information and communication between fixed and mobile endpoints, whether it be a command center or an individual in the field.

The primary products and services include:

Government mobile broadband products and services provide military and government users with broadband and multimedia connectivity in key regions of the world. They are the sole provider of all government travel aircraft like Air Force One and Marine One

Government satellite communication systems, offer a wide array of mobile and fixed modems, terminals, and access points designed for manpacks, aircraft, UAVs, seagoing vessels, and ground-mobile vehicles.

Secure networking, cybersecurity, and information assurance products and services, provide HAIPE-complaint encryption solutions that enable secure military communication over networks.

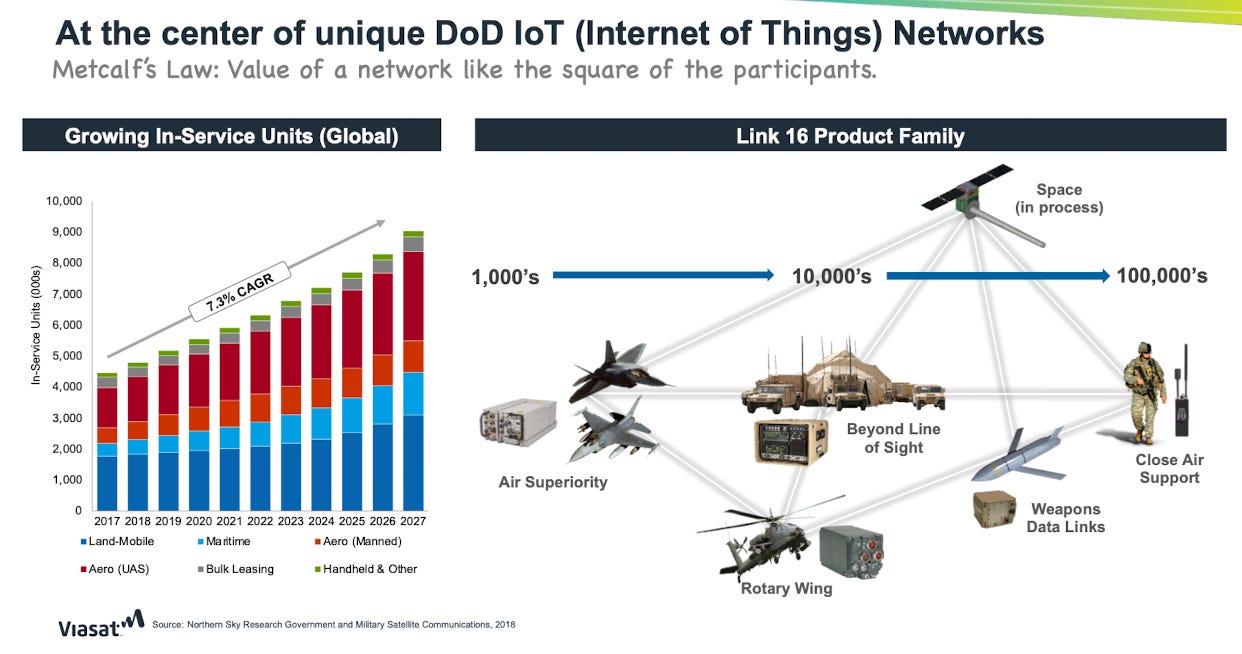

Tactical data links, including the BATS-D handheld Link 16 radios, STT 2-channel radios for manned and unmanned applications, “disposable” defense data links, and the MIDS and MIDS-JTRS terminals for fighter jets.

I know those read like a bunch of letters and don’t mean much on the surface so this should help visualize what these terms mean.

Think about how sticky a product like this is. Once the terminal is in the UAV or a fighter jet the odds of it coming out are slim.

Capital Cycle Overview

It would be a remittance of me to not take the time to discuss the prominent capital cycle in this business. Every 5-7 years VSAT has launched a new satellite and grows its network. The cyclicality of this can be seen in the financial statements during these times. Before launch, the leverage ratio increases and capital expenditures increase.

From the outside, this can look concerning if you are not willing to dig deeper into the company and see where this spending is going. Each new satellite requires more investment in not only the bird itself but in the infrastructure to support the demand. It’s nice to have an expensive satellite in the sky but if there is nothing on the ground then it doesn’t matter.

In an interview on the ValueWalk Podcast, Cove Street Capital’s Eugene Robin discussed their thinking behind their VSAT position and the first question Eugene was, “Why now?” And the answer had entirely to do with the capital cycle.

Around the time of the Viasat-2 launch, (June of ’17 and was put in service Valentine’s Day ’18) construction began on the third generation. During Fiscal Year ’18 they spent around $500 million in capital expenditures and today this number has grown to about $2.5 billion in Capex. This constellation alone will cost the company around $2-2.5 Billion to build.

We are currently towards the end of the investment cycle with the first satellite completed and is currently in prelaunch testing on the ground with Boeing, the second is close to this point, about 6 months away, and the last one is about 80% there. The whole constellation is expected to be in service in around 3 years with a cash flow inflection point 3 quarters after the second satellite launch.

To get an idea of the potential ROI of this heavy Capex investment I took a look at the previous spending in the lead-up to the Viasat 2 launch.

1/ Viasat-1 launched in October of 2011 and it took until June of 2017 to launch the second generation

2/ During that time span they spent around $1.94 Billion on Capex

3/ Measured from the time it was put into service (20181Q) they have generated an additional 1.712 Billion in operating cash flows. (I use OCF because they use EBITDA and I am not a fan in this situation)

4/ Given this time frame of 4.5 years we are looking at about a 15% annual ROI.

These are the numbers I have been using for the VSAT 3 constellation and there is an argument that the ROI could be greater due to some of the costs being eliminated thus expanding the margins.

Industry Overview and Economics

VSAT, boiled down to one simple term is a supplier of broadband. They sell internet access and connectivity to individuals who can not get it from a cable. This is a new type of market and when I think about new markets the first question I have is, “How big is it?”

According to the estimates we are currently looking at a Trillion dollar market that is expected to increase by 50% over the next 10 years. VSAT has exposure to all of these segments with competition in each of them but they can be mainly broken down into two categories. Governmental competition and Non-governmental.

This section in their 10-K describes the situation better than I could.

“In our satellite services segment, we face competition for fixed broadband services both from existing competitors and emerging technologies. Our fixed broadband service offerings compete with broadband service offerings from wireline and wireless telecommunications companies, cable companies, satellite companies and internet service providers. Many of our competitors are larger than us, have substantial capital resources, have greater brand recognition, have access to spectrum or technologies not available to us, or are able to offer bundled service offerings that we are not able to duplicate, all of which may reduce demand for our broadband services. In addition, the broadband services market continues to see industry consolidation and vertical integration, which may enable our competitors to provide competing services to broader customer segments.”

Non-Governmental Competition

Hughes- Biggest competitor in residential broadband. They have 1.5 million subscribers and have produced revenues of 1.5 billion through 2Q21. Own the Juniper fleet of GEO satellites, in terms of economics, they are the closest to competing with VSAT on a cost-per-bit basis with Juniper 2 coming in at $2.5 per bit. Viasat-2 has a cost of $1.8 per bit. Link to investor relations: https://ir.echostar.com/events-and-presentations

Intelsat- Large competitor, owns 52 GEO satellites in the C and Ku spectrum. Acquired GoGo and became the largest in-flight Wifi provider. They filed for voluntary bankruptcy in May 2020 but produced revenues of 1.9 billion in 2020. 2020 10-K link: https://investors.intelsat.com/static-files/751e73fa-453a-43fb-9b78-a491d9e4d011

One Web- A LEO competitor that exited bankruptcy recently with the backing of Softbank and Hughes. After bankruptcy, the backers put in $2.7 billion to make it work. They are not public but the website: https://oneweb.net/investors

Amazon- Recently threw its hat in the ring with the Kuiper network. Are planning to launch two satellites with a lunch date TBD but this project is backed by Amazon which has deep pockets.

Starlink- The biggest noise maker in the industry is Elon’s Starlink. He plans to launch almost 40,000 LEO satellites, there were only 2,000 in the air as of recent reports. It’s hard to see much more than what he says in public and on Twitter but this is a viable competitor in the residential broadband market.

Governmental Competition

Hughes and Intelsat both have government businesses that have backlogs of contracts

The large defense manufacturers like Northrop Grumman, General Dynamics, and L-3 Communications.

Other government communication service providers like Raytheon and BAE systems.

Like addressing the TAM earlier they list the majority of the competitors in their 10-K, in reality, though there is only a handful that competes with VSAT on a product-by-product basis. But there is something that stick out when assessing the competitive landscape: The majority of these competitors have deep pockets and the ability to burn money for a long time.

In a growing industry and with the forces of capitalism at work, only the strongest will survive, and having deep pockets with the ability to take pain for a long time can be extremely valuable for a venture like satellite communication where you might not see positive returns for years on end with the need to continue investing. We have already seen some big consolidation and moves towards vertical integration to prepare to build companies that can fight strategically in the industry. There is a big TAM and there are quite a few companies that want a slice.

LEO vs GEO

In the satellite world today there is a long debate going on that compares the use of Low Earth Orbit satellites (LEO) to the use of Geostationary satellites (GEO). Here are the pros and cons of each.

Low Earth Orbit

Pros

Requires much less upfront capital to build

Can launch thousands of satellites compared to a few GEOS

Because it is lower to the earth, it needs less power to work.

Low price ground equipment is sufficient for ground stations.

Has shown better latency characteristics for real-time applications

Cons

Covers less of the earth per satellite

Because they are only visible for 15-20 mins the signal gets handed off to another satellite making it hard to test and troubleshoot one satellite.

Atmospheric effects are greater causing disorientation.

Have a smaller life span of around 5 years

A littered history of bankruptcy. When Elon was asked about Starlink he said the goal was to, “not go bankrupt.”

Geostationary

Pros

Satellites are visible for 24 hours giving constant signal without any handoff needed.

There is a less number of satellites needed to cover entire earth (only 3)

A much longer life span of around 15 years

Ideal for broadcasting and multipoint distribution because it stays fixed.

Cons

It takes massive capital upfront to build

The signal takes longer to travel to earth due to it being higher in space. Thus it is hard to use for real-time applications like playing a video game or streaming live video

Limited coverage to one specific region.

Less redundancies should something go wrong, they are not easily replaceable.

I am in the camp that there is no black and white answer for which is a better system. I believe it is a mix of both. Satellite broadband will not be a winner take all market. I believe over the coming years a few of the strongest will survive and when the competing taps out they will eat up their share. But when it comes to LEO vs GEO there is no clear-cut winner and I don’t think there will be. It will probably be a mix of both.

The analogy I use is that of a cargo ship. The bigger ships can ship each container at a lower cost per container compared to ones with a smaller land size, but the smaller ships can move faster, thus creating an opportunity and someone out there will always want speed.

Demand For Bandwidth

None of the above matters if there is no demand for his supply that is coming online.

The above points don’t exclusively apply to the VSAT but rather the industry as a whole.

Since the invention of the internet, it has been a large adoption to include it in our daily lives and it is becoming more and more like a product similar to electricity and heat. I wouldn’t be surprised if these companies are treated this way in the future.

We have lived through the shift from being offline to being online with everything we do over the past 20-30 years and this writer is confident this trend of adoption and demand for bandwidth continues into the future. COVID likely pulled forward a few years of demand so I wouldn’t be surprised if the demand numbers bounce sideways for a few years but when you take a step back and look at it as a whole the base rates for this trend to continue are good.

Doug Dawson wrote an article outlining the state of demand for the industry and analyzed the average monthly U.S. household broadband usage.

“The amount of data used by the average broadband user has been doubling roughly every three years since the advent of the Internet. This exponential growth has been chugging along since the earliest dial-up days, and we’re still seeing it today. Consider the following numbers from OpenVault showing the average monthly U.S. household broadband usage:

1st Quarter 2018 215 Gigabytes

1st Quarter 2019 274 Gigabytes

1st Quarter 2020 403 Gigabytes

1st Quarter 2021 462 Gigabytes

Average household usage more than doubled in the three years from 2018 to 2021. The growth happened at a compounded growth rate of 29% annually. That’s a little faster than the more recent past, probably due to the pandemic, but the compounded annual growth rate was around 26% in the decade before the pandemic.”

(Source: https://circleid.com/posts/20211013-explaining-growth-in-broadband-demand)

Satellites have a cost advantage when it comes to bringing the internet to rural towns and homes that are not served by tractional cable providers, plus, there is a market for connectivity to places where laying fiber cable is not an option, like 10,000 feet in the sky or in a tank on a battlefield. When compared to fiber cable, however, they stand no chance but a company does not build satellite broadband to compete with fiber.

Moat Analysis

What you see in the satellite broadband industry right now is capitalism at its finest. A large somewhat-new addressable market where this going to be a lot of dollars spent and a bunch of competitors racing to capture as many of those dollars as possible. You love to see it right?

Viasat has strategically positioned itself within the industry so they have a large moat around their business.

1/ The culture of innovation and engineering is top of its class. Before Viasat-1 there were no high throughput satellites and the entire industry ran on Ku-band. After inventing the first Ka-Band satellites the team at VSAT proved their ability to innovate for the future. I believe the best way to explain this moat is when Hughes stole their intellectual property needed to build high throughput satellites for their Juniper 1 satellite. Viasat sued and won over $100 in legal awards, with the case showing a long paper trail clearly showing patent violations. Copying is the best form of flattery. (Link to article: https://spacenews.com/41781loral-agrees-to-pay-viasat-100m-to-settle-patent-suit/)

2/ The Government business is a beast. I briefly led to it above but the Gov’t business is one of a kind. Think of these data link systems as the Trojan horse for VSAT. Once these links are put into military vehicles, they’re not coming out and once the third generation constellation is up, they can sell bandwidth directly without needing to lease it out to competitors.

At its core Viasat is a defense business, this is how they got their start. Over the decades it has taken what it developed for the military and has developed it for commercial and residential customers. In its most recent 10-K, the firm showed a backlog of $2.3 billion, with have expected to be delivered in the next twelve months. 90% of this backlog is done through fixed-price contracts.

3/ Right now they are one of the lowest-cost producers in a commodity environment, once Viasat-3 is in the sky, they will be the lowest cost producer by a wide margin and the technological innovation is one of its kind. The ability to be the lowest cost producer and offer the best product in terms of bandwidth capacity is a huge advantage when it comes to negotiating contracts: “We can give you 2x the capacity for the same price as the other guy”

4/ Part of the secret sauce to having a satellite broadband network is the ground infrastructure. Due to the vertical integration VSAT has been able to produce the top-of-the-line hardware for their own networks and as the “space industry” continues to grow it opens them up as being the supplier of choice for the equipment needed to run a reliable and high-speed network through satellites.

5/ Viasat-3 will be a revolutionary product offering a Tb of bandwidth and increasing the capacity of the VSAT system by a factor of 8. In addition to having more capacity, the coverage will now be global allowing them to be the first global broadband satellite provider, and this global coverage, from a US-based company, is a big advantage for the government alone.

6/ Flexibility and optionality. This is a double-edged sword. The ability to shift capacity to where the demand is desired gives VSAT the advantage of not being pigeonholed by any one line of business but the lack of specific focus could leave room for competitors to come in and completely focus on the one niche.

However, with this large flexibility leaves the seeds for optionality and by listening to the customer first, a culture they have embodied, they can shift attention and focus to those given desires. We have seen them enter and dominate verticals, IFC as an example, and with all these options the future could turn into a number of possibilities. Right now, there are plenty of lines in the water between residential fixed broadband, community wifi, IFC, Gov’t, maritime usage, or just selling the hardware.

VSAT is not a one-trick pony. They are building an ecosystem that can adapt to changes in demand and meet those demands quicker than their competitors, thus the opportunity for growth.

Management and Incentives

Behind an innovative company is the founder who embodies the word innovation to their core. As far as this writer is concerned, Mark Dankberg is one of the greatest innovators of our time. He got his start at a little know company called Linabit which is now a division of L3 Harris. But the alumni network has gone on to found a large number of technology companies, one of the most well-known is Qualcomm.

Mark co-founded Viasat in 1986 with his partner Mark Miller, who is the executive vice president and the chief technologies officer. Mark has been the CEO since day one but recently stepped down from the position and gave it to Rick Baldridge who has been the COO since 2000. Now, Mark is the Executive Chairman which to me means his job now entails everything about the future and he has little to do with the day-to-day operations of the company. His job is to dream and steer the ship.

Mark, in the truest sense of the word, is a visionary leader which has its pros and cons for an investor. The pros are that he comes into work every day with the long-term mindset of what the company will be doing years from now and positioning the company to make those moves in the present. The cons of this are he isn’t very talented when it comes to investor/public relations. He doesn’t care much about the stock price, all he cares about is the business and what it’s going to look like 10 years from now.

When Rick came in as CEO there have been some better improvements to make sure VSAT is being as transparent as possible for investors and to the public. Mark has been seen in more interviews and since stepping away and every quarterly earnings report now comes with a short shareholder letter updating investors about the nature of each business unit and the overall picture.

Some other notable character in the company is the COO, Kevin Harkenrider, who earned the title recently. He sat down to discuss the upcoming year for VSAT on their own company podcast. You can find it here: (Link) in it he makes it clear the goals for the year are to focus on getting the first bird into service and make sure everything on the ground is ready when the capacity comes online.

Another interesting individual is a gentleman named Doug Abts, when you look up the leadership team he is on the first row of individuals right next to Mark and Rick, but he isn’t well known anywhere else. His title is “Senior Vice President Strategic Planning and Corporate Development. In his profile, the role is described as,

“In this role, he is responsible for implementing the Company’s strategic vision through business performance planning, competitive environment review and prioritization of financial/non-financial resources around strategic investment opportunities.”

Previously he has a lot of M&A experience and has been involved in the strategy of the company since joining in 2015. A little bit about his background, he graduated from Harvard Business School and did his undergrad at Stanford, and from 1995 to 2001 he was was an Operating Officer and Platoon Commander in the Navy Seals. The guy is a badass and he is head of strategic development for the company.

Compensation

When it comes to the incentives of the company, they pay their executives using a simple structure. Each receives a base salary, a bonus, some stock, and then options. The options are the most interesting because the sole performance metric is the total shareholder return over a 4 year period compared to the S&P Midcap 400 Index. If they are below the 25th percentile of performance, no options will vest and be forfeited by the executives. They are very clear about how this works in the Proxy:

“The performance-based stock options awarded to our executive officers are designed to further align executive pay with stockholder value creation by only delivering value when Viasat’s TSR during the applicable measurement period outperforms the TSR of at least 25% of companies in the S&P MidCap 400 and Viasat’s stock price exceeds the exercise price of such performance-based stock options.”

This happened for executives for the last four years when 1) the relative performance was below the 25% and the exercisable price on the options was above the current market price on the date. They felt the pain, which I am sure was the driver behind the recent efforts to start being more transparent to investors with the quarterly letters, more interviews, and the media efforts like the podcasts and the blog.

When scanning the options table in the Proxy there are a few thoughts that come to mind. Most of the executives especially Mark and Rick have options with an exercise price ranging from 60 to 70 in the next five years but the grants from the calendar year 2020 are the interesting ones. Because they vest on a 4-year rolling schedule, the options earned 4 years from now have an exercise price of $35.66 and the number of them is significantly more than in prior years.

For example, in 2019 Rick was compensated with options to buy 122K shares at a price of 71.83. Last year, he was comped with options to buy 305K shares at a price of $35.66. Most of the executives have this similar setup with the 2020 compensation and around 1 million shares were granted through options with an exercise price below $36 which is about 1.25% of the compani’s shares outstanding.

Mark currently owns the most stock out of everyone, he owns about 2% of the company he founded. In a founder-led world today this is a low number but he gains ownership through his options and stock grants. All in all, Directors, officers, and management own around 5% of the company. The largest shareholder is Seth Klarman of The Bauopost Group, and he owns 22% of the entire company, and has a “board observer” title, and is allowed to sit in on the meetings and I am sure they ask for his thoughts on matters.

$1 Dollar Test and IV CAGR Calc

This company does not pass the $1 test. I use cash flow from operations here because the company has a messy income statement and I believe it is hard to get the full picture using Retained Earnings. They don’t pay out a dividend and over the past 5 years, they have not bought back any stock so all of the cash has gone right into the business.

It has been a rough 10 years for VSAT shareholders. If you were to look at the price movement alone, at the time of this writing looking back 10 years gives you a dead money result. The price peaked in May of 2019 at $90 a share but hasn’t touched those levels since then and didn’t bottom out until December of 2020 at around $33 a share.

Over the past 5 years, we have seen a nice IV CAGR of around 14%. Again I used CFFO instead of Net Income or EBIT because it was easier to get a gauge and I didn’t want to use EBITDA. The company has been free cash flow negative for a while because of the huge CAPEX for the satellites but management has pounded the table with the guidance that there will be a cash flow inflection a few quarters after the launch of the second satellite. So we will see, try explaining that to the shareholders who have been holding for 10 years with nothing to show of it.

Headwinds

1/ The industry is new with wide competition and these competitors have deep pockets. It’s one thing to fight against a cash-strapped startup that is in a fragile state but it’s another to fight against someone who can continuously raise money for years in the effort to take market share. To finish first, first, you must finish and if you have an endless war chest that time frame can expand immensely.

2/ At the end of the day, Viasat is strapping $1 billion to the top of a rocket and sending it into space. There is a blow-up risk which could be absolutely devastating. The base rates point to this chance being around 3% but management has stated the 3% runs on the high side.

3/ The GEO vs LEO battle will go on for another 5 to 10 years and we will only see which is better with the passage of time. I am willing to put money down that the answer is somewhere in the middle with a blend of all the orbits together.

4/ Regulation, there has been a massive push for space regulation. The question becomes, whose problem is it? And with the growing risk of space debris, this regulation could be closer on the horizon than we think and rules regarding launching and satellite positioning slots could affect the entire industry.

5/ The industry dynamics right now don’t have good base rates for shareholders. It is an all-out war to gain and establish market share in this new industry and to do that companies have to fund their programs one way or another. We have seen Viasat use the public markets frequently and have diluted shareholders considerably over the last ten years. But one can not expect to see a shrinking share count or a focus on shareholders while competitors are aggressively fighting for market share and scale. Usually the former comes after industry consolidation and the winners emerge.

Tailwinds

1/ The size and growth of the TAM mean this will not be a winner take all market and there will be several companies who can compete within the subsections of this TAM. With VSAT having the option to pivot into the areas where demand is needed the most gives them the strong ability to compete in the markets where they have an edge. This ability to pivot will be crucial in an industry so competitive right now.

2/ Strong balance sheet and large shareholders. The company has been run somewhat aggressively if we are to look at the leverage ratios. The way management uses leverage ramps up into satellite launches and then scales down after launch. We have seen VSAT do this before and so the likelihood of them successfully executing the playbook once again is high. The other big thing they have is the “500-pound gorilla” in the board room but not on the board. Seth Klarman owns 20% of the company. This gives management the ability to fight off potential raiders. Plus, having one of the best value investors in the world as a “board advisor” could help them see capital allocation in a new light through osmosis.

3/ With the launch of Visat-3 they will be the first global GEO player who will be able to offer coverage around the world and overseas for IFC, which has never been done. The Government systems business will also benefit immensely from the now global coverage. It will offer new revenue streams which were nonexistent and brand new to the industry in general.

7/ Vertical integration will allow them to capture more of the dollars spent on the space industry than if they were not involved in every step. Like selling the equipment needed to run a ground network to other companies.

5/ Viasat has a strong operating history and long relationships with customers more specifically the government. These long relationships have led Viasat to become the provider of broadband on all of the travel vehicles for the Gov’t and they have been able to build a durable moat around their business with the Tactical Data Links in the warfighters and handheld radios for the military. These moats are deep and with each new node in the network, it becomes more valuable. Maintaining this relationship will be key to VSAT’s success and they have shown they are able to keep the customers happy.

6/ Their new constellation will make them the lowest cost provider in an industry dominated by commodity-like characteristics and the ability to deliver more for less and better for less can put them in a position to dominate the markets they wish to play in.

Final Thoughts

I found Viasat last year around this time. It was through a Podcast with Ben Claremont and he mentioned the name so I took a look. I thus spent the last year studying the company and the dynamics in which they are playing. All in all, I think Mark is one hell of a visionary when it comes to connecting the world through broadband and the Viasat-3 constellation will shake the industry. His focus on the business over the last ten years and neglecting the shareholders has tested the patience of those who have held during this time frame, Seth Klarman being one of them. The earliest I could find him buying VSAT was back in ’09. But with this being said there is a tipping point on the horizon.

They have spent the last 5 years pouring money in capital expenditures into this new satellite constellation and when it is in the air it will be the biggest thing for this company since buying the first satellite back in 2009. This will be the biggest jump for them as they move out of reaching critical mass and transition into being able to fund Capex with cash flows from operations with enough free cash flow left over to return to shareholders. They have not stated this but I am sure there has been talk given by the “board advisor”.

The biggest uncertainty right now is the competitive environment. We have seen the other dogs in the race exegete and they are to be respected. There are a lot of things going well for VSAT right now but I would not bet against Elon Musk or Jeff Bezos. They have the ability to go on for years without needing a single dime of outside capital, a huge advantage. But I wouldn’t count out Mark either. He might not be as famous as the other two but his expertise in the area of satellites puts him up there with the best.

The next couple of years for the company will be interesting. With the satellites they now have control of under the new merger with Inmarsat (I will be wiring an entire article on this later) and Viasat-3 going up in the air to give them global coverage, management has stated the five-year goal is to double revenues and more than double EBITDA during that time frame. Should this happen, VSAT will look like the biggest competitor in the satellite connectivity space.

Disclosure: I am long Viasat

Please be advised, Wall St Gunslinger is not an investment advisor and does not give personal investment advice. All content is for educational and entertainment purposes only. Investing entails a lot of risks and should be managed appropriately. Please do your own research and consult with an investment professional before making any investing decisions. Thank you.