Occidental Thoughts

I've owned the name for about a year now, here is my current stance and the variables I believe will drive future returns

Disclosure: I am long OXY

The first time I was ever interested in Oil and Gas was during the heat of COVID when the price of oil dipped negative. Although the fear was understandable during that precious time, I thought there was a bit of an overreaction and there could be some opportunities.

At the time OXY was one of the names that was crushed and because I am a glutton for punishment, I got interested. More specifically, the 7-year warrants with a strike price of $22 were trading around $7-10. These looked appetizing and my curiosity led me into a study of the oil industry. In the end, I bought some in the winter of ‘21 and held for about 6 months.

I am not proud of the next sequence of events.

After stagnating around $10, my shiny object syndrome led me to sell the warrants because I convinced myself Oil was out of my circle of competence. Here is the comical part, I bought $BABA with the proceeds. I thought I understood an e-commerce company on the other side of the world better. What a clown.

Either way, I learned my lesson because the warrants are now trading for $40 and BABA went from $170 to $80. Thankfully, I pulled the plug before the name saw the bottom. I couldn’t take the pain and the conviction wasn’t there. Apparently, I have to touch all of the hot stoves in this game.

It was about a year after I sold the warrants that I circled back to the name. Reflecting on the initial purchase, it was a risky buy and I am not convinced I had a firm understanding of the level of risk I was underwriting. There was a real solvency question and I disregarded it because, to me, the price was so cheap.

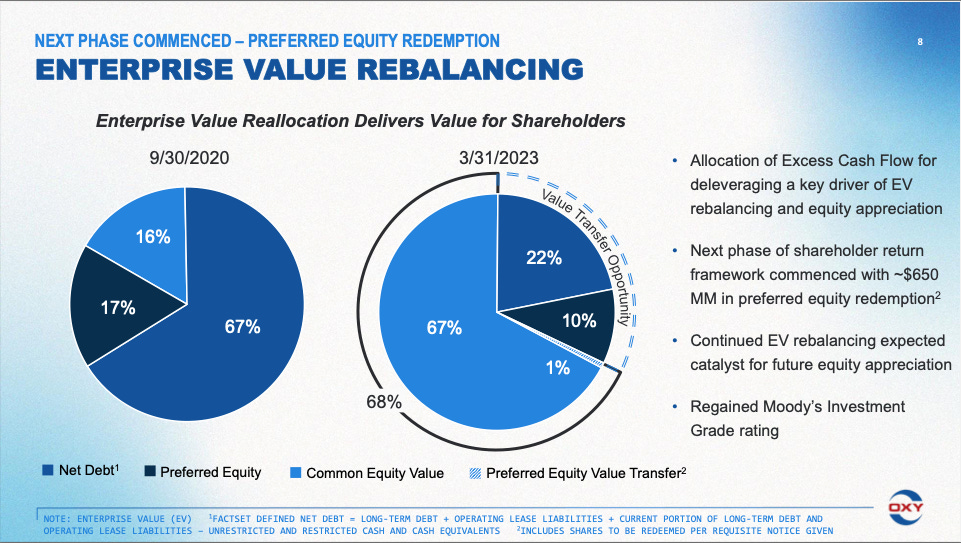

Today, the reality at OXY is quite different after the rise in Oil prices from late ‘20 to ’22 helped the company produce enough cash flow to stabilize their balance sheet and give common equity a much larger share of the pie. As you can see the simple strategy of paying down debt has ~tripled the common equity in the company since September of 2020.

I am still pondering the effects of this “Enterprise Rebalancing” but I feel as though the long-term effects from this strategic move will be felt years from now and could be underestimated in the short term.

Right now, OXY is the largest landholder in one of the most prominent oil basins, which one could argue has become more valuable to the US based on recent world events. They are also one of the lowest cost producers in the basin with a breakeven of around $40 a barrel and an industry average of around $54.

We have a low-cost producer in one of the best basins in the world that has been hell-bent on returning capital to shareholders instead of pouring it into CAPEX and M&A.

Now the latter point is ongoing. This is where the discrepancies between investors occur. Some think it is only a matter of time before the industry gets M&A and CAPEX crazy, while others believe there will be less investment in operations and more shareholder returns. I fall into this camp.

I purchased OXY because I believe the majority of the cash flows generated from the company will be returned to shareholders in the form of repurchases, dividends, and debt repayments.

The company today trades with a market cap of ~$57B and an EV of ~$75B with an investment-grade credit rating. In ’21 and ’22 oil averaged $68 and $98 and on those prices, OXY generated $7.5B and $12.3B in FCF respectively. Close to 100% of this cash was sent back to shareholders.

I calculated shareholder return by adding net debt issuance, net share issuance, and dividends paid.

If this trend of capital return continues and they can average $9-10B in FCF on a $57B market cap, the yield is 15%+. Not bad.

These results will be lumpy with the change in commodity environments but the important variables here are:

The low-cost operational position

The large ownership of prime “real estate”

The commitment to shareholder returns through buybacks, debt repayments, and dividends

If these stay at the forefront of the company then the long-term prospects, in my opinion, will be fruitful for owners of the common. It also helps that management’s pay is linked to cash return on capital employed, total spend per barrel, and relative total shareholder return.

Please be advised, Wall St Gunslinger is not an investment adviser and does not give personal investment advice. All content is for educational and entertainment purposes only and should not be interpreted as anything other than such. Investing entails a lot of risks and should be managed appropriately. Please do your own research and consult with an investment professional before making any investing decisions. Thank you.