Markel, A Wise Man's Stock

A look into the 3 characteristics that define both, Tom Gayner and Markel: Simple, Consistent, and Restrained.

A business becomes a reflection of the people who flip the switches and the Markel Way could also be the philosophy in which Gayner lives his own personal life.

I have long admired the guys over at Markel, but I have never taken the time to sit down and conceptualize the company. It never stood out to me.

To me, there was always a better opportunity or a better idea to spend time with than sleepy, old Markel.

What made it stand out now? Maybe because I am becoming sleepy and old myself.

There are quite a few high-quality characteristics that Markel embodies but hyper scaler, fast growth, and rocket ship are not them.

In the story of the tortoise and the hare, Markel is without question, the tortoise.

But don’t let looks deceive you.

Markel is by all accounts a compounding machine with 3 engines creating value:

Insurance

Investments

Ventures (Wholly owned non-insurance subsidies.)

You won’t catch this company doing 26% a year CAGRs or making you rich overnight. This stock isn’t putting you on a beach in a year.

It might in 40 years, though.

During my study 3 overwhelming characteristics stood out to me; Markel is simple, they are consistent, and they show restraint. If one wants to understand the company as a whole, they have to understand these 3 principles.

Simple

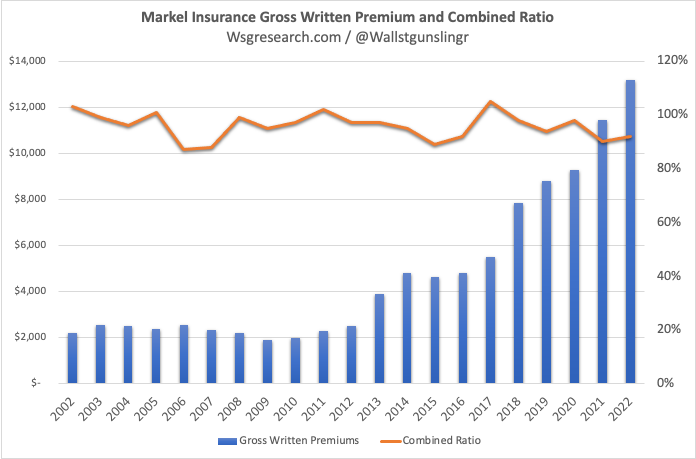

Insurance

In 1930, Sam Markel started an insurance operation to cover Jitney Buses.

Since then, Markel has gone on to expand its operations into lesser-known portions of the insurance market where they have become the leading underwriting in niche lines that other, bigger companies, won’t touch like:

Equine mortality,

Summer camp liability

War and Terrorism risks

Hole-in-one insurance

Errors and omission coverage for professionals.

These lines of coverage are more complex.

You can’t call up GEICO, State Farm, or Progressive to get a quote. This specialization has led them to have domain knowledge of these complex little markets that other insurance companies won’t touch.

This specialization has been profitable and is part of the competitive advantage.

Investments

The success of the insurance operation means there is money left over at the end of the year to invest. A positive cycle that feeds itself.

If you write good insurance, you can invest, if you can invest well, you can write more insurance…….

“Basically, we’re a hedgehog that knows one big thing. If you generate float at 3% per annum and buy businesses that earn 13% per annum with the proceeds of that float, we have figured out that’s a pretty good position to be in.” - Munger

Their investments sit in two baskets, fixed income and equities.

The fixed income is structured to match the potential liability claims they might have in the coming years and once that amount is met, the rest is invested in equities.

Tom has been the head of the investment portfolio for decades at Markel. As of the most recent earnings call, the Markel portfolio has outpaced the S&P by 1% over the past 30 years. Might not seem like much but over that period of time equates to a lot.

“We remain 100 basis points ahead of that index for over 30 years. We don't usually move ahead during sprints, but we do tend to outlast the competition when it comes to marathons.” - Tom Gayner on 2Q23 Earnings Call

When selecting investment for the Markel portfolio Tom looks for 4 things.

Good returns on capital without too much debt.

Run by managers with equal measures of talent and integrity.

Reinvestment opportunities and capital discipline.

At a reasonable valuation.

This probably sounds a lot like Buffett and Munger, and it should, with one small difference.

Tom manages the portfolio for Markel in a different manner than the way Warren and Charlie run Berkshire. There are no big swings but rather a consistent effort to buy into great companies at a fair price.

The way he invests the portfolio runs in the same rhythm that he does everything else.

Don’t try to shoot the lights out, do a little above average, and do it for a long time. It does achieve incredible results.

The equity portfolio is currently worth ~$8.3B with ~$5.3 being unrealized gains.

Ventures

In 2005 the company launched its venture portfolio with the acquisition of AMF Bakery for $14 million. As of the most recent quarter, the Ventures portfolio today produces about ~$5B in revenue and ~$620M in EBITDA, which Tom Describes as the least-worst proxy as a way to gauge profitability.

The move into non-insurance subsidies is one we have seen before and I expect the total revenue from ventures to climb well into the future. The move has opened up an entire runway of capital reinvestment for the company in a more tax-efficient way.

As of the most recent 10-Q, for the first 9 months of ‘23 ventures has produced $474M in EBITDA, compared to $353M for the same time period last year.

The Flywheel

The three engines of growth for Markel are all intertwined and have the ability to compound on one another through the years.

The order of allocation is insurance, tuck-in or acquisitions within ventures, equities, and fixed income, and then if there is still capital left over, buybacks.

Buybacks have been a bit popular as of late

On the surface, it is a simple strategy but difficult to get right. Based on the results, it’s hard to argue they haven’t been moving in the correct direction.

Consistent

Ambitious CEOs strive to be the Michael Jordan of X. Maybe Bird, Magic, or Kobe.

Tom chose Cal Ripken, Bill Russel, and Lou Gehrig.

All of these players were not outstanding in one area but their endurance amplified their results and made them legends.

At the beginning of his life, Gayner’s father made the realities of the world clear to him,

“There’s always somebody smarter than you. There’s always somebody taller than you. There’s always somebody faster than you. There’s always somebody you know has more talent than you. So at the end of the day, what you should focus on is your work ethic and showing up and participating in something that is not necessarily the talent that’s going to distinguish you. It’s not height, it’s not speed, it’s not those sorts of things.” - Tom Gayner on RWH

From then on, the game became more about endurance than any one-year outcome and this has become the story of Markel.

The company is not well known for its huge growth rates, monster acquisitions, or exciting new business lines.

For Markel and Gayner, business is not a sprint, it’s a marathon. The winner of a marathon is the one who slows down the least.

That is the focus, show up every day and push like hell to put one foot in front of the other. If one can do that over decades magical things can happen as reflected in their business results.

Using the most recent 20-year clip the company has produced the following results:

These are not earth-shattering but they are not horrible either.

Over the years Markel has not been defined by horrendous losses in one year and incredible results in another, rather they have consistently shown up, achieved a respectable record, and have done so for decades.

One step at a time.

Restrained

The investing style in which Tom runs the portfolio for Markel draws many comparisons to how Buffett structures Berkshire except for a small detail.

Buffett has been known to take big swings and sit for decades and Gayner maintains a more diversified basket of investments with his largest position being ~11% of the entire portfolio (Which happens to be Berkshire).

He gets a lot of questions about this from individuals who want to know, “Why don’t you concentrate more?”

To which he replies along the lines of, “I am not as smart as Buffett and the positions we hold are big enough to make a difference but not big enough to kill us”

When I was younger this answer didn’t satisfy me.

Besides, isn’t wide diversification for those who don’t know what they’re doing?

I have changed my stance on this.

It is likely that those who end up studying Gayner’s approach are those who have been burned by a more aggressive one and are now seeking comfort.

It is only after touching these hot stoves and losing money for myself, that I now appreciate what Gayner has been able to do and how his long-term incentives are aligned more by casting a wider net.

Those who seem to progress the most are the ones who have the ability to stay away from extremes and be satisfied with those results.

To say Gayner, “doesn’t know what he is doing” or “lacks conviction in his own ideas” would be foolish. You do not produce the track record he has by being foolish.

He knows what he is doing and he is willing to restrain himself because there is redundancy with diversification that adds another layer of protection to Markel that isn’t quantifiable.

Yes, this might give up a few percentage points a year but if the goal is to ensure the long-term success of Markel, then it is a price worth paying.

If the business is a great one, there will be plenty of opportunity to buy into it over time and the concentration will grow with the increase in share price.

Again, this is a marathon.

This type of self-control has been the driving force for stable long-term performance. They do not indulge in the extremes and this has kept them away from shareholder destruction in the form of bad investments or bad underwriting.

If Tom tried to push he would have opened Markel up to more risk, and to him, it isn’t worth it.

You have to admire someone who knows their limits and stays within them.

Markel is the wise man’s company

A wise man is someone who would rather understate their ability in an effort to make sure they don’t overstretch. It is someone who focuses on the downside first and knows the upside will take care of itself over time. We have seen this trait before in other great investors like Howard Marks and Seth Klarman.

Tom Gayner runs in the same rhythm as them.

Tom does not look to shoot the lights out with big acquisitions or a highly concentrated stock portfolio. He focuses on minimizing the risk of loss and works each day to become a little bit better.

When I was younger this didn’t appeal to me. I wanted something that was going to make me rich, fast.

I wanted the stock that was going to 10x in 10 years. Something I could hang my hat on.

But this effort brought me into higher-risk, money-losing scenarios. There was no downside focus, I was more concerned with how much could I make vs how much could I lose.

I was not wise.

Today I see investments through a different light.

Instead of focusing on the upside, I am much more concerned with the probability of loss and durability. These are not sexy traits and they don’t make you rich overnight.

But they keep you from becoming poor.

This is why MKL has become more attractive to me over the years.

Their ability to keep things simple, stay consistent, and show restraint has nicked the ability to outpace the broader market over the last 30 years. In any single year, there was not a huge amount of outperformance. But the margin of victory doesn’t matter. What matters is a victory nonetheless.

Investors would be better served if they too embodied the principles taught at Markel.

They might not make you rich tomorrow, but they will keep you out of trouble.

Disclosure: A family member I speak with owns shares of MKL 0.00%↑

Please be advised, Wall St Gunslinger is not an investment adviser and does not give personal investment advice. All content is for educational and entertainment purposes only and should not be interpreted as anything other than such. Investing entails a lot of risks and should be managed appropriately. Please do your own research and consult with an investment professional before making any investing decisions. Thank you.

Thanks for your article, its interesting for me to hear this view as I come from a typical concentrated, high conviction philosophy.

I wouldn't say that I am convinced that diversification is the way forward. I strongly believe in investing in your top 5/10 ideas (risk-rated), rather than trying to invest in 100 companies and beat the index slightly on average. Perhaps I am wrong, but I am curious about your perspective when you weigh the 2 strategies, because if I would want to diversify and protect my downside, wouldn't you just buy the index?

Thanks for this write up, Michael. I learnt a lot about Gayner's philosophy.

It's interesting to see several superinvestors add to their MKL positions this year.