Frontier Temperature Check

We still see continued execution on the fiber build but is the debt level beginning to cause some concern?

Since I wrote the initial post in March there has been one large question floating around in my head: Where are they going to get the cash to continue the build-out of their fiber network?

I am worried they are going to have to rely on the market’s appetite to fund their growth engine rather than use internal cash flow. Thus, putting the execution of their strategy in the hands of someone else.

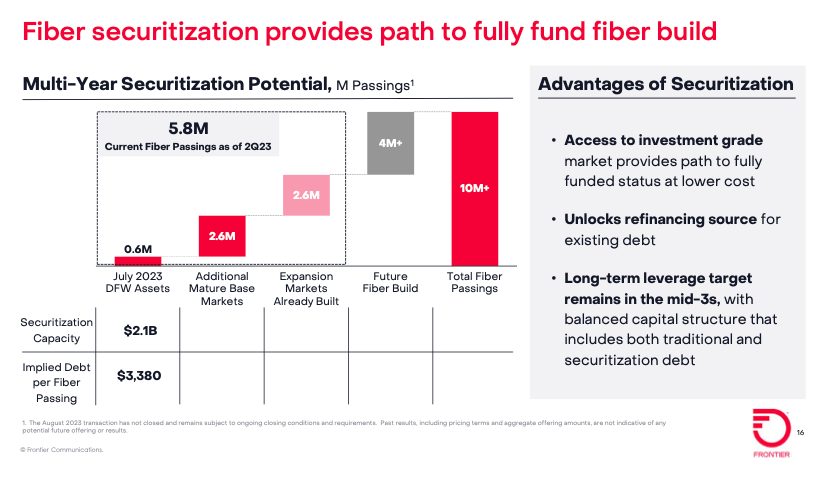

This one focus has been the topic of some serious thought and it didn’t make it any easier when they raised more debt using the fiber assets in the DFW area as collateral during the last quarter. After the raise, their leverage ratio peaked at 4.1x trailing EBITDA, which is up from a 2.8x multiple from only 12 months ago.

They target to run the company with a mid-3s ratio and I think that is respectable given the asset and how other peers run their operations. Right now they are on the higher end of the ball park but if EBITDA grows through the rest of the year it will come back down.

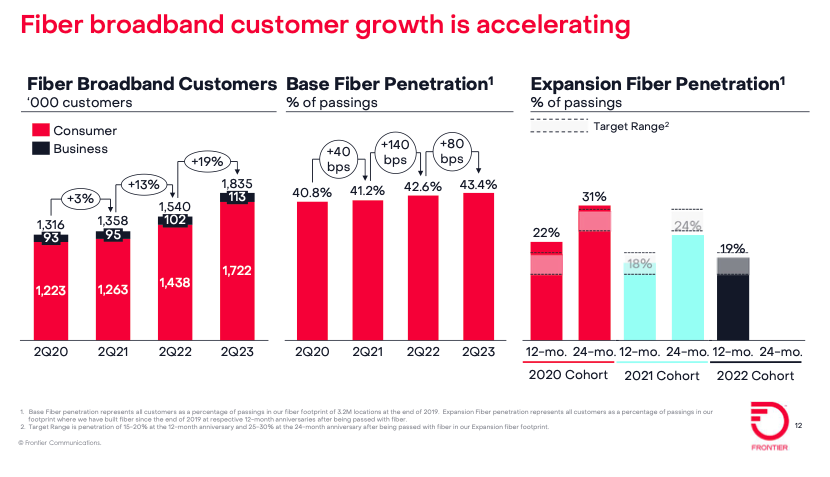

The operating metrics of the fiber builds are running in the right direction, they have grown fiber customers by 20% YoY and fiber EBITDA continues to push higher at a healthy clip. The turnaround is continuing to move in the right direction as the company becomes more and more fiber focused as each day passes.

As the company continues to swap out copper customers with fiber ones the overall economics of the business are going to begin to heavily reflect the higher margin profile of the fiber subscribers and grow the value of the company in the long run.

I am still pondering the 2nd order effects of raising the capital to continue the build-out. From where I stand today the market seems to be playing with this puzzle too. If the company was sold I think it would be able to fetch a premium, but the majority of the value resides in the future as they continue to build out the fiber network and attempt to bring penetration rates up in the markets they already serve.

There are a bunch of risks when you couple future-led value with relying on debt markets to reach your destination that doesn’t make me feel warm and fuzzy.

For now, though, the continued growth of the fiber customer set has me optimistic. The company has guided that CAPEX will be lower here in the latter half of 2023 as they eat up the working capital already spent in the build and inventory levels come down.

If the company is able to continue to add fiber subscribers and grow cash flow, I find it hard to throw in the towel yet. If the signal is the number of subscribers then we are on a good path. If they undermine their own success by overloading the company with debt, it could spell bad news. With the most recent raise and the leverage ratio hitting a new high, I will be paying close attention to the balance sheet moves for the rest of the year and if they continue to raise debt and fiber customers stall or slow, I might have to pull the plug. For now, though, I am going to continue to sit tight.

The question to me is, what is the more important variable, the growing number of fiber subscribers or the debt load? I am still working on an answer but I know where my gut leans.

Please be advised, Wall St Gunslinger is not an investment adviser and does not give personal investment advice. All content is for educational and entertainment purposes only and should not be interpreted as anything other than such. Investing entails a lot of risks and should be managed appropriately. Please do your own research and consult with an investment professional before making any investing decisions. Thank you.

Clear and concise update, thanks for sharing Michael.

- Alex