Boot Barn Rough Dive

Dipping my toe into the Yellowstone effect

I came across $BOOT on a screen from TIKR. Yes, I do use them. To be quite honest there are little things I love to do more than bring up a screen with ROIC or ROE >15% and then just go down the rabbit hole. It feels like a treasure hunt. On this particular day, $BOOT came up with an ROE of the TTM of around 38% and it caught my eye. Before last year, well really before 2020 I would have probably seen the name and made a quick pass. Even now I was hesitant to double-click, but I did. I have a deeper familiarity with the store now that I didn’t then.

About two years ago I got my first pair of cowboy boots. It is without reservation that I confess the initial purchase was around the time of my 24th birthday and I had been watching Yellowstone Season 1 at the time. Did the show nudge me? Yes. Since then I have been a loyal fan of both the Dutton Family and to my cowboy boots.

Back at the end of April 2022, I was in Nebraska and when my parents wanted something to do I thought there was no better way to be more Omaha than to head over to a local Boot Barn. I walked in empty-handed and came out with another pair of boots and a few pieces of turquoise jewelry for my girlfriend. We were both happy I went.

With these thoughts running in the subconscious I came across the name and felt the little twitch to check them out from a place of genuine curiosity rather than a real idea of finding what could be an investment. When I pulled up their financial statements though, I quickly found I wasn’t the only one watching Yellowstone.

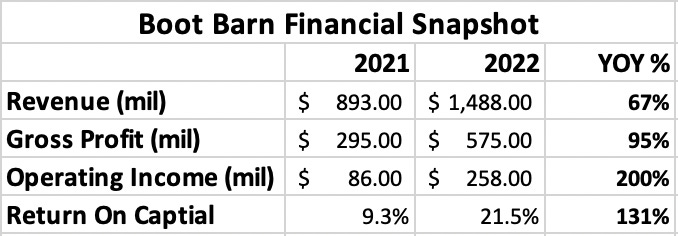

Whenever I see a result like this the skeptic in me rises right to the top. Immediately my brain is thinking this is a one-time phenomenon and that these levels are not sustainable. I mean look at these changes in some key metrics YoY.

Now when I come across a retailer or restaurant I have this mental model I call, “The Black Box”. It’s the simple way I think about it in terms of understanding the unit economics, if I can understand the operating nature of one box, then I can somewhat get an idea of how the financials with this company will look as they place more boxes around the country. This is rough but I refer to being vaguely right than precisely wrong.

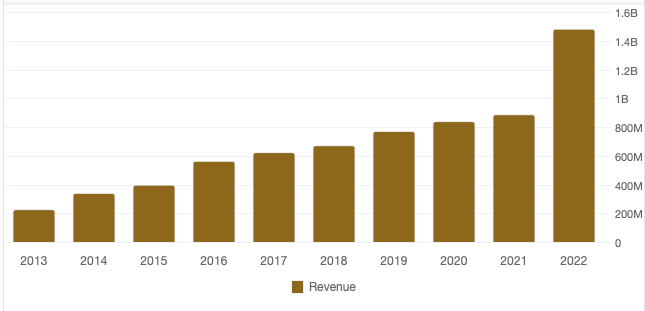

Financial Overview

With the numbers from above in mind I went through the rest of the financials and was pleasantly surprised at the operating metrics of this company even if you take out the massive growth year in 2022, we have consistently growing revenue, gross margins between 30-35%, operating income growing pleasantly year over year, their operating margins before 2022 weren’t much to write home about, around 6.5-9%, but they have been growing EPS at around 20% a year for the last 5 years in 2017 they had an EPS of $.53 and in 2021 it was $2.01.

When it comes to the quality of the earnings produced I compare the operating income to the cash flow from operations as a way to see if they are using accounting engineering to mislead investors, a “look over here” trick used more often than I am happy to admit.

They are around the same. In 2022 they made some huge investments in inventory (who didn’t?) but they are within the ballpark of each other when you look beneath the surface and can trace back the #s to how they differ a small amount.

On the balance sheet side, they have a debt-to-equity ratio of around .5 and they haven’t massively diluted shareholders over the past 5 years with diluted shares outstanding only growing from around 27 Mil to 30 Mil. They have a Net Debt of EBIT multiple of less than 2x which doesn’t scare me away.

Rough Unit Economics

Now, these were printed in the earnings presentation but I went through and did my own numbers because I feel like they are a bit excessive. I don’t feel comfortable using these numbers as my “base rate” so I went back to 2021 to get an idea of the unit economics then.

Just to explain why in this slide, they said a new story payback of 1.4 years and in the 2021 Annual Letter Jim Conroy said this:

“New stores opened this past year have exceeded our sales plans and are expected to pay back within our targeted 3-year period or better. “

Which one is the more appropriate one to use for estimates? I chose the lower one. Anyway here is the unit economic breakdown for the past few years using store count, total sales, and EBIT Margins to find the EBIT per store. This I think gives the investor an idea of how much earnings one location can produce.

Where is the Puck Going?

Since their first public report in 2015, every annual letter comes with 4 main tenets and they have been the same for $BOOT from the beginning. The growth and focus of Boot Barn will come from these 4 pillars:

1) Driving same-store sales growth

2) Strengthening their omnichannel capabilities

3) increase the penetration of their exclusive brands

4) Expand store base

In 2015 the company had 170 stores across 26 states and did around $400 Mil in sales and every letter that has been written every year after that has come with the same 4 tenets of growth. When I see this I think of a few things.

1/ They are really focused on this formula and so far it seems to be paying off in regards to their preformance, revenues have been increasing steadily since their IPO.

2/ It says something about a CEO repeating the same thing year after year. Maybe at this point, he just copies and pastes the same words and just changes the numbers to reflect the most current year. I am not sure if this would be a red flag or not.

I do have some questions though about the second to the last paragraph of the annual report:

“During the last couple of years, we have worked to expand our customer reach to a more casual country lifestyle customer in addition to our core western and work customers, and as a result, we believe our total addressable market has increased from $20 billion to $40 billion. The expansion into this country's lifestyle segment has further increased the opportunity for Boot Barn to grow its national footprint, and we are confident that our U.S. store count can triple from its current base to 900 stores. This is very exciting news for the Company as we continue to expand the brands’ reach across the United States.”

If you are the CEO of a company, how can you write with the conviction that your total addressable market has doubled and on top of that you think there is room to expand up to 900 stores, tripling your store count of today? It just seems crazy to me. Why didn’t you just keep pushing forward as normal and continue on the path you have been traveling since the start? Opening new stores, increase revenue, increase earnings, rinse, repeat? Why do you have to go out in the annual report after a massive year and make a statement like that? It just seems to me that it is the opposite of underpromise and over-deliver. Now you have a huge target and the expectations are much higher, so I hope you’re right.

The growth in sales to me seems to come from a tailwind of the Yellowstone effect. How long will it last? I am not sure but hopefully, it is long enough to grow the store base that large.

Whenever I size up a company I tend to not only weigh the track record of what has happened in the past but I wouldn’t be a true investor if I didn’t think about what this name looks like a few years from now. There is an ever-present thought between where we are now and where could this be headed.

Here are some of the eventual realities I played out on a notepad when looking at BOOT 0.00%↑

This is what revenues and EBIT look like if we break down the numbers into per-store metrics. (This is a rough estimate)

2022: Total revenue was $1.5 Bil, with around 300 stores, that’s $4.5 mil per store with EBIT coming in around 420K per store per year. I got all of the sales numbers and margins from TIKR. If these numbers can remain constant this is what the future looks like:

500 Stores @ $450K EBIT/Store = $2.25 Bil EBIT

750 Stores @ $450K EBIT/Store = $3.37 Bil EBIT

If we use 2021 sales #s and the EBIT Margin was about the same of 10% we would have around $3.2 Mil in sales per store and 320K in EBIT / Store. Using these numbers we get:

500 Stores @ 320K EBIT = $1.6 Bil EBIT

750 Stores @ 320K EBIT = $2.4 Bil EBIT

The Total Enterprise value of the company today is trading around $2.5 Bil. When you look at these numbers there are a few scenarios where today’s price looks like a bargain like if they are able to one more store rapidly and do higher numbers in them than on the 2022 print. Would I bank on that? No.

If we are using history as any guide, in 2015 they had around 170 stores and at the start of 2023, they will probably be in the range of 350 which is an annual growth rate of around 10% a year so double every 7.5. years, if they keep on the current pace we would see 500 stores before 2027.

Final Thoughts

When I think about $BOOT and its future of it I believe the tale is being told as we speak but I am not confident enough to do a really deep dive into the company just yet.

The biggest resason I see for caution is it feels like a fashion trend that has been pushed onto the masse by a hit TV show, one which I love and pushed me to buy my own pair of boots. But the one question that reigns above them all is this level of sales and performance sustainable over the coming years. I am just not confident it will be and if the level of sales falls per store, EBIT follows and this throws off any kind of analysis of the company.

I will leave on a positive note though if they are able to maintain their new store payback period between 1.4 years, which was stated in their most recent earnings call, and 3 years, which was stated in their 2021 annual letter, that IRR ranges from high 40% to 26% and anywhere in that range is an acceptable compounding rate if you ask me.

I’ll be keeping this company in the back pocket and checking on it periodically, probably every couple of quarters, mainly to see the sales numbers. I am to ready to dive deeper but I am more than curious to keep an eye on it.

Peace and Love,

Michael

Please be advised, Wall St Gunslinger is not an investment advisor and does not give personal investment advice. All content is for educational and entertainment purposes only and should not be interpreted as anything other than such. Investing entails a lot of risks and should be managed appropriately. Please do your own research and consult with an investment professional before making any investing decisions. Thank you.