Ballantyne Update

Progress report

It’s been about 4 months since I published my initial BTN deep dive and about 6 months since I sat down to write about the company. Since the initial article, there has been enough movement to warrant a little bit of an update on the business and how it is progressing.

Listen to the podcast that goes along with the article:

The last article ended with the idea that this thesis revolved around capital allocation. There was enough evidence prior to the initial investment to give me confidence in the leadership to create shareholder value in the long run. This, and the fact that at the time of purchase the company was trading for a little less than the market value of its 2 public equity investments and the carrying cost of its 1 private investment (which might be worth more than it is carried for on the balance sheet). This price did not include the operating portion of the business which I can say with a degree of confidence is worth more than $0.

Operating Business Update

Earlier this year shareholders were told that management was seeking a way to separate the operational business from the company and it was going to be done through an IPO, not a spin-off. There were a few questions, why do this instead of the spin-off? Why not just keep the business in-house? I am willing to accept the argument that these moves were calculated and are being done to unlock more shareholder value than just a spin-off.

Here is the gist of the plan:

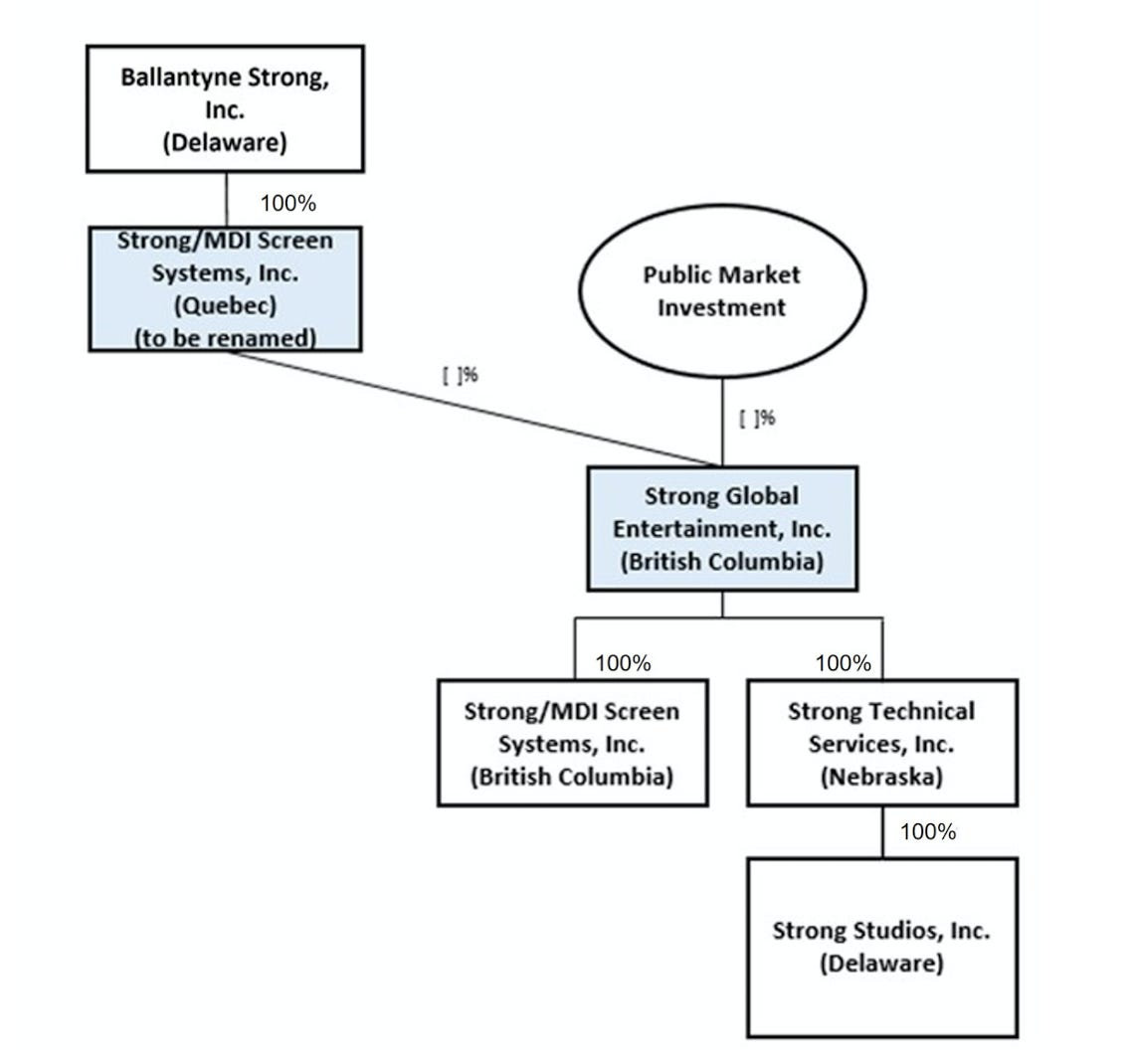

The company going public will be named “Strong Global Entertainment” and will trade under the ticker “SGE” here is a chart from the S1 which shows what the organizational chart looks like now pre-IPO and what it will look like after.

Before:

After:

At the end of the day, the company will be majority-owned by Strong/MDI Screen Systems Inc, which is going to be renamed. Are they taking requests? Because of the way the org chart looks, I think Blue Chip Screens would be fitting.

Looking at the financials has given us much more of an idea as to what was lying underneath.

Here are the numbers that I am paying attention to (Listed: fiscal ’20 and ’21)

Revenues: $20.8m - $25.9m

Gross Profit Margin: 22.3% - 28.4%

Income from Ops: ($1.3m) - $1.2m

Cash Flow From Ops: $4m - $4.8m

FCF (CFFO - CapEx): $3.5m - $4.4m

The new company will have $8.8m in equity so the FCF to shareholders equity gives us a return of about 50%. Not too shabby.

If I was to ballpark a valuation around this business I’d have to say between 8 to 10 times FCF and I think that’s conservative. Given the companies leading market position, strong relationships with the customers, and a few growth drivers this could prove to be ultra-conservative but I could be wrong so I’ll air on the side of caution.

Here is how I am thinking about this whole situation. When I put my owner’s cap on, BTN currently owns 100% of this entity. As we can see it’s throwing off around 4m in cash flow each year with a solid market position and a few growth drivers. This IPO is going to give BTN an inflow of cash through the sale of ownership. I hope leadership wouldn’t go out and sell a portion of the company we own for less than its intrinsic value which I would conservatively ballpark at $32 to $45 million.

If we see the growth drivers like Strong Studios, which already has a revenue guarantee of $9 with the completion and delivery of the projects, the eclipse screens, more services revenue from cinemas upgrading their equipment, and the enormous cinema backlog from COVID come full circle, the estimate above could be super low. I would rather have low expectations and be surprised. We saw promising results in Q1 ’22 with revenues for the first three months being ~$10m and a Gross Profit Margin ~25%, this revenue was over 100% compared YOY to Q1.

We still don’t know when the IPO will go forward or at what price. There was mention on the most recent conference call about waiting for the right market environment. I am willing to guess this means they will not be doing it while the S&P is close to being down 20% on the year. The appetite for stocks is lower than it was late last fall and thus, who knows how long we could be waiting. Given the strong showing in Q1, waiting could benefit shareholders in the long run.

Investments Update

FGF Financial: 25% ownership with a current market value of $4.65m. FG has been successful in raising two new SPACs and we all see what these turn into.

GreenFirst: ~9% Ownership ~25m, GreenFirst reported a strong Q1 ’22 earnings with an EPS of $.18 per share, and with BTN’s ownership of 15.3 million shares, we get look-through earnings of $2.754 Mil (This is all in Canadian Dollars). BTN acquired the stake for about $16 Mil (CAD). In Q1 alone they got a 17% look-through return on their investment. This kind of performance and housing demand statistics has me hopeful for the rest of the year.

I should also note Intefor, another large lumber mill, took a 16% stake in GreenFirst. I am going to assume the management at Intefor knows more about the sawmill business than I do so I’ll take the action as a bullish sign. But I could be wrong.

FireFly: a $13 million investment under the cost method which is now carried at $12.8 million due to, I am assuming, an amortization write down that is done with every cost method asset of the balance sheet whether it is depreciation or amortization. They have currently made a partnership with Hyundai to have them on their screens in the car for professional drivers. This enables drivers to bring in more types of income rather than just lift fees. Overall, I think this holding is more valuable than the cost that currently represents it on the balance sheet.

Cash at the end of the quarter was ~8 mil.

Add all of these up and we get a value of $50.45m not including the screen business.

Final Thoughts

As we come near the middle of 2022 we are starting to see the fruits of the labor management has done over the past couple of years. In terms of capital allocation, I am pleased with the progress so far. I am looking forward to seeing the % of SGE that gets sold to the public and at what valuation. This will be a great test to see how well can management drive shareholder value in the long term.

When I look through the investments they look to be firing on all cylinders with no new surprises. It seems like everything at GreenFirst is starting to come around and given the favorable market environment it is pleasing to see them turn a profit so early in their “operating” history. Firefly and FGF have nothing new to report. FGF was able to raise two new SPACs, continuing to execute on the strategy they have discussed at length, and in Firefly’s case it’s nice to see them partner with a large car manufacturer and continue to grow the business. It would be nice to get an update on the operations of the business but given the VC nature of the company, I wouldn’t expect to see anything.

The SGE segment is looking to benefit heavily from the movement back into a “normal” operating environment since COVID. The tailwinds behind them like the movie backlog and cinemas pushing to upgrade their systems could give them a boost after a lot of pain over the past two years. The content segment is going to be an interesting one to watch. I don’t know much about the movie business but I am happy to see leadership will not be throwing money at a movie blindly. The fact that they were able to broker a minimum revenue guarantee was nice and makes me believe that even if this turns out to be a flop, it won’t rip our face-off. I am okay with the company taking calculated risks to push for more revenue streams as long as the downside doesn’t sink the ship. So far, the company has done nothing to lead me to believe they would ever put themselves in such a predicament, and consummating a deal with an MRG was enough evidence for me to believe so.

The ongoing movie (get it?) that is BTN, which will soon be named FG Holdings, is continuing to play out. A few things I will be paying attention too for the remainder of the year:

1) The SGE IPO price and % of the company sold to the public

2) What is management planning to do with the cash received from the sale

3) The progress of each of the investments

So far I am pleased with the progress made. Shareholder value is created over multiple years and we are only at the start of the game.

Peace and Love,

Michael

Please be advised, Wall St Gunslinger is not an investment advisor and does not give personal investment advice. All content is for educational and entertainment purposes only and should not be interpreted as anything other than such. Investing entails a lot of risks and should be managed appropriately. Please do your own research and consult with an investment professional before making any investing decisions. Thank you.